Michael Jordan cited: “Get the fundamentals down and everything you do will rise”

In a world where everyone on twitter or youtube seems to be an expert in equity markets, it gets important for us to not get distracted and focus on what might actually help us in wealth creation.

Hi everyone, to bring back the basics, here on Multipie, we will dig deep & start the following series:

- Financial statements analysis

- Company analysis

- Business valuation

- Personal finance

Warren Buffett quotes that “Accounting is the language of business”. Every financial number is a starcast in the evolving movie called the business.

Hence it’s important to understand what role every starcast aka financial number is playing in informing us about the business! Trust us its not as simple as calculating a few ratio from annual report. An annual report is approx 100-300 pages and every page conveys something relevant about a business.

Outline

We will begin with Financial statement analysis, but first things first, Why financial analysis is important?

In this section we will connect all the dots of annual report and explain the ideal way to understand, compare & analyze each & every line item in financial statements of any company which will help you judge how to discover quality businesses.

This series is brough to you jointly by Finnacle Academy and Multipie

—————————————————————————————————————————

In first edition- Financial statement analysis series we will be starting from 1st and most important line item- Revenue and in this post we will cover: “Understanding Presentation & Calculation of Revenue Figures – Part 1”

What is revenue?

Revenue a.k.a topline/total income is sales (turnover) of a company, generated from its business operations during the year. Companies earn revenue in return for the supply of goods/ services.

Why understanding revenue & its drivers is important?

- It’s the only sustainable source for the co. to generate cash to fuel the growth & survival of the business.

- Revenue leads to earnings (after deducting costs) & earnings drives valuations (we will cover this later that how earnings drive valuations)

Thus, understanding Revenue figures and its drivers is very important as whole business and valuation analysis is dependent on revenue among a few other factors.

Presentation of revenue is different by different companies in different sectors

E.g: Have a look at revenue reported by a FMCG co. v/s a bank in annual report- FY21.

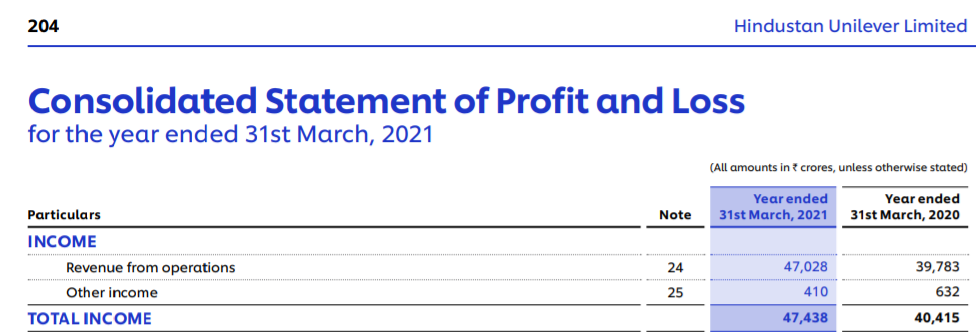

HUL:

ICICI Bank:

We will be understand separately in detail how BFSI companies report financial statements differently than a manufacturing co.

How is revenue calculated?

Total Income/Revenue from operations = Revenue from operations + Other Income

In HUL’s case: Total revenue from operations (total income) = Addition of revenue from Operations and Other Income i.e. 47,028 + 410 = 47,438 Cr.

- Revenue from Operations: Income generated from the company’s core business operations.

Now to understand, how this core revenue of 47,028crs is generated one needs to open the revenue’s footnote number adjacent to the revenue figure (footnote no. 24 in HUL’s case) in the annual report.

Sales of products/services = Sales price (Contract price) – Trade discounts/ volume rebates – Sales returns – Taxes/ Duties

Sales Price/ Contract price – Price at which the good/ service is sold/ rendered respectively

Trade discounts – Discount offered to retail customers

Volume Rebates- Discount offered to customers for buying in bulk volumes

Cash discount- Discount to customers if customers pay advance/ full cash payment on invoice date for the entire goods bought/ services availed.

To get more clarity on how revenue is exactly recognized, one should read the revenue recognition policy of the company. E.g of HUL in the snapshot below:

Under new accounting standards, it is mandatory for firms to disclose a breakup and computation of Revenue from the Contract price (sales of product & service). Look at HUL’s contract disclosure:

- Other Operating revenues – Incentives/income which company receives only because of its business operations. It consists of:

- Export Incentive: Generally offered by Governments to encourage industries to export their products or services globally/ to a selected region/ country.

- Claims Received: A claim is an official request as part of insurance or other legal claims for payment which the company demands for the goods which are usually damaged

- Sales tax incentives: Excemptions/ Refund of the state sales tax if co. is engaged in product categories like renewable energy equipment etc.

- Interest subsidy: Amount that the government is offering to incentivize the borrowers for conducting their operations

For example Interest Subsidy for MSME Units in Gujarat: Through this scheme, an interest subsidy of up to 7% for micro-enterprises and 5% for SMEs is provided.

2) Other Income: Let’s take a look at what falls under the Other Income item on the Income statement from footnote 25 in HUL.

Interest Income: is classified as Other Income (i.e. Non-Operating Income) unless you are in the Banking industry and its core business.

Dividend Income: is classified as Non-Operating Income unless you are a holding company i.e. it’s your business to invest shareholder’s money in some other companies and grow them.

Conditions of when hedging gains & FVTPL (Fair value throughP&L) is included in other income and when in other operating income will be covered later.

Now that we have understood how companies present and calculate revenue figures, the question is, should we take their reported Operating revenue as Revenue for our analysis? No!

In our next post, we will cover how to understand the adjustment that needs to be done to make revenue numbers useful for analysis.

That’s it for Part 1. We will also be organizing discussion sessions for each chapter