Hey there!

A very good morning from Team Multipie! We present you another edition of Multipie Weekly, where we share recommendations to watch, read and summarize the week gone by.

So grab a cuppa of your morning drink and let’s get started!

Outline

The Week (and month) Gone by…🗓

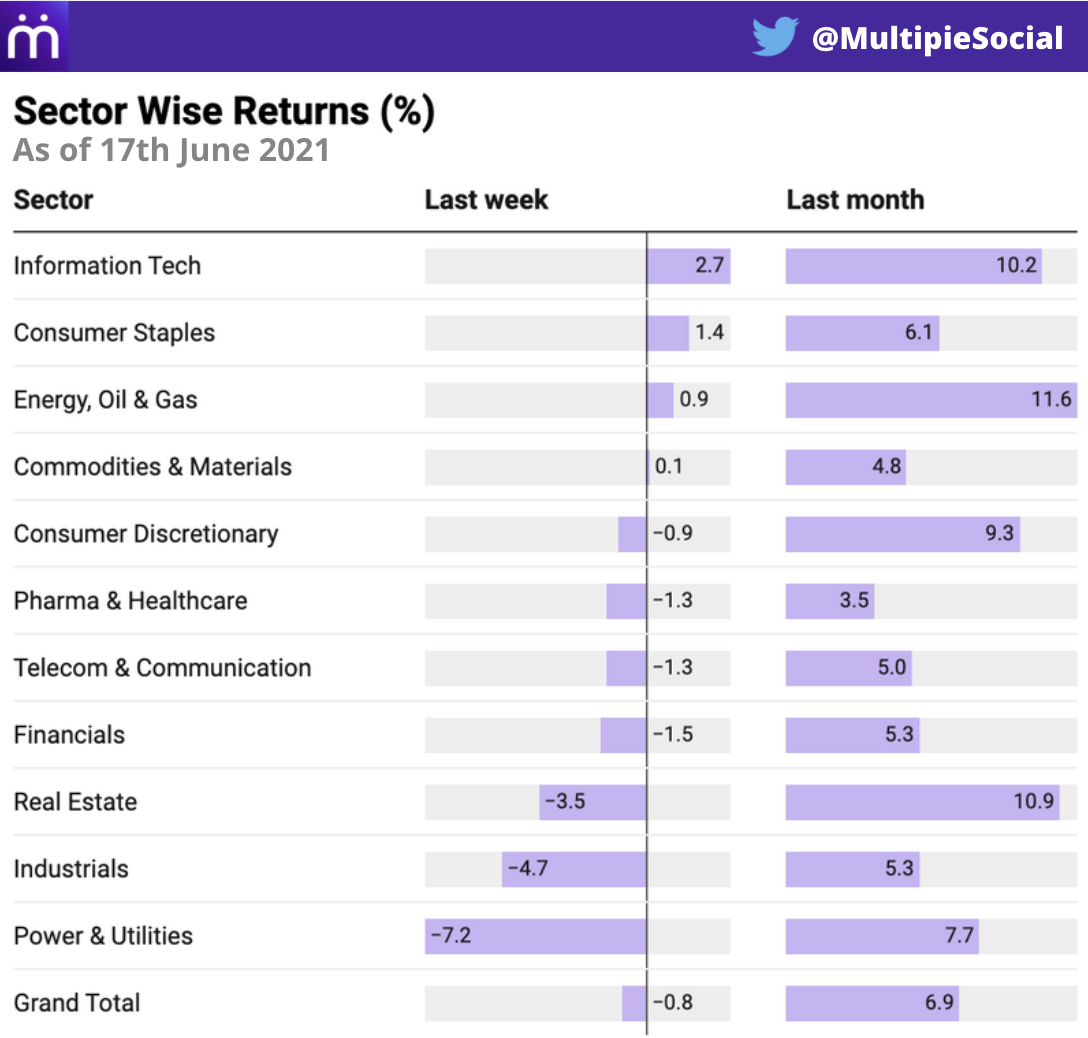

Last week, Indian markets felt some jitters after the Adani controversy and closed in red territory with minor retractions.

Let’s dissect the week gone by via a snapshot of sector wise returns. Similar to last week IT was one of the few sectors in the green joined by Consumer Staples & Energy. On the other hand, in stark contrast to last week Power & Real Estate saw a substantial correction.

The market continues to see strength in Micro & Small caps, while Mid & Large caps saw minor weekly corrections.

A history of bull markets in India and where do we go from here

‘The lessons of history’ by Will and Ariel Durant carries a timeless quote – “Most history is guessing and the rest is prejudice.” This week we look at the history of previous bull markets in India and compare it with current one, trying to guess the way forward, while keeping the prejudices in check. We referred to a note by Morgan Stanley in framing our takeaways below. But remember – History rhymes, but rarely repeats.

Takeaways:

- There have been 6 bull markets since 1990; Criteria – Sensex should double

- Excluding the super bull market of 2003 to 2008 that lasted close to 5 years, average duration of other 4 bull markets is 72 weeks (~1.4 years); Current bull market that started on March 24, 2020 has lasted 64 weeks.

- Morgan Stanley believes that the current bull market is similar to 2003-2008, given a likely new profit cycle

- While we may see further upside in the immediate 12 months, the pace of gain may slow down

- As against common perception of current rally being ferocious, the average weekly return is at 1.7% which is lower than the average of previous bull markets’ weekly returns at 2.8% (2.0% excluding ‘91 – ‘92)

- India has outperformed Emerging Markets in each of the previous five bull markets with an average outperformance of 52% versus 23% for this bull market. Morgan Stanley expects India to continue to outperform EMs in the coming months.

- Current rally is led by Cyclicals (Commodity, Industrials and Consumer Discretionary) with underperformance of Financials being an outlier

- Top sectors as per MS for the coming year are Consumer Discretionary, Industrials and Financials

- While Nifty trailing P/E is close to peak P/E of previous cycles, there is more valuation comfort if one looks at P/B (MS thinks it is a better metric, given the impact of the pandemic).

- Significant upside can be expected on FII flows even from here.

- Takeaway: MS believes this bull market is here to stay for longer.

Comparison of Bull market cycles:

Source: Morgan Stanley; edited by Multipie

Visual representation of previous bull markets:

What do you think? Are you a bull or a bear – let us know!

SPAC that! SEBI Plans Framework for SPAC Listings

SEBI is strongly inclined towards allowing the listings of SPACs – the shiny new market instrument that caught US markets’ fancy last year. Earlier this year, it tasked its Primary Market Advisory Committee to create a structured framework for the same.

What are SPACs?

SPACs or Special Purpose Acquisition Companies are simply ‘shell’ companies with no operations. However, these are publicly listed for the sole purpose of raising capital to acquire an existing company.

How do SPACs work?

What do the SEBI developments imply?

- Currently SEBI has a profitability criteria for companies to list. This move would allow “unicorns” which are not able to meet the profitability criteria for IPOs to raise public capital through SPACs.

- The Advisory Committee also realised the need of protecting retail investors and minority shareholders. As a result, it is expected that mostly institutional investors will be allowed to invest in such companies and retail participation will be limited.

- There is still a long way to go before SPACs are allowed to list. New laws and regulations will be required to ensure these “blank-cheque” companies do not have corporate governance issues.

- However, this is a welcome step towards modernising and expanding Indian capital markets. But, SEBI must also consider allowing “Direct Listings”. The trio of IPOs, SPACs and Direct Listings are essential to make capital markets attractive and competitive.

Outlook is Bullish for Capital Intensive companies

Last few years might have made you believe that asset light models and platform companies are the only future. Well, Ian Harnett of Absolute Strategy Research disagrees, and he does so with sound logic in his article for the Financial Times.

Here’s what we found interesting from his piece:

- Main factors driving his outlook are the COVID 19 induced stagflation risks and the governments’ response to push demand and full employment

- Four key basis for outperformance of capital heavy business models:

- Scope for reshoring

- Shift in investment from information to infrastructure

- Need for climate efficient infrastructure

- Investment in technology required for geopolitical dominance

- Global infrastructure requires a whopping $94tn investment to keep up with demographics and replace ageing infrastructure for times to come.

- Climate & carbon efficient infrastructure will need to be built for sectors other than the EV industry as well, be it steel production or agriculture.

- The ambition of geopolitical leadership will compel countries to invest in technological research & innovation which will further add to creation of capital heavy models.

How can this play out in India?

- The fact that most companies are investing in Technology reduces competition for Capital heavy players.

- Given India’s ‘Aatmanirbhar’ ambitions and initiatives such as Production Linked Incentive (PLI) scheme focused on manufacturing, we think capex heavy sectors are enablers as we traverse the path from an emerging to a developed economy

- While reshoring and an information to infra shift might NOT be as prevalent in India, we face a critical void when it comes to climate efficient and geopolitically competitive infrastructure. This will need to be filled soon if we are to attain global leadership.

TATA Digital: On path towards a Super App

Tata Digital made the news yet again this week! The company continued to add verticals and compelled us to dedicate a piece to it.

So what is Tata Digital building?

A ‘super app’. Now you may ask what that is? A super app is nothing but a digital ecosystem that will provide its customers with all the products and services they may require. This is similar to what Amazon or WeChat built in the US and China respectively.

Why is this relevant?

You might know that we covered Tata’s acquisitions of 3 startups last week, but an ET article tells that TaTa Digital is even planning to add a financial services vertical to it’s super app!

Currently, the company’s recent acquisitions of 1mg, Big Basket, and Cure.Fit have indicated that the app would be supported by a strong portfolio of product offerings.

The Tata group already has a presence in AMC and Insurance businesses. It is also speculated that Tata might even apply for a banking license once RBI allows corporate houses to apply.

It is worth noting that Tata has tied up with HDFC Bank, Kotak Mahindra Bank, Mastercard, Flipkart and even NABARD to apply for a new umbrella entity(NUE) license for a pan-India retail payment network.

Implications:

These developments indicate that Tata Digital is soon going to be a force to reckon with globally.

Since Tata Digital is also eyeing acquiring or partnering with neobanks, it will be interesting to see how the Indian fintech startup space unfolds!

Chart of the Week

Our chart of the week – The cost of 1 GB of mobile data in every country.

The cost of mobile data in India stands at the lowest in the world, and this makes us wonder about the headroom for ARPU improvement for Indian Telcos.

Jefferies report

Every ₹ 10 increase in ARPU is expected to add ₹ 2,500 crores to incremental EBITDA of Bharti Airtel!

Courtesy: Visual Capitalist

In Other News

- The US Fed kept it’s interest rates unchanged at near-zero and forecasted a hike by 2023

- The RBI gave an “in-principle” approval to a consortium of Centrum Financial Services and BharatPe to take over PMC Bank, paving the way for it’s resolution process. We believe this is a big win for Fintech in India. While PMC depositors get comfort on the safety of their deposits, this gives @bharatpeindia will not just be a re-seller for Banking products, but have a Small Bank license of their own!

- Twitter has lost its intermediary status and has had to face some unwanted consequences as a result of non-compliance with the Indian government’s new IT policy

- Paytm has called for an Extraordinary General Meeting (EGM) on July 12th to approve a fundraising plan of Rs. 12,000 cr ahead of its IPO

- Don’t forget to catch the Day 3 of India v/s New Zealand for the inaugural World Test Championship Final

Please share with your peers if you found this helpful and subscribe at multipie.co to start receiving these as a weekly digest every Sunday

Wonderful and so helpful content.