Rakesh Jhunjhunwala holds a stake worth approximately Rs. 10,500 crores in $Titan Company Ltd today. However, this journey traces back two decades when he decided to invest in the then underperforming stock.

A thread 🧵

2/n

How did he identify Titan to be a multibagger?

In the early 2000s, $Titan Company Ltd faced a range of challenges

1. A key factory in Hosur had been shut due to a dispute between the management and the Employees’ Union which led to a hit on the profitability of the company.

2. Prices of raw material, such as gold increased steeply.

3. Not only had competition increased but demand had become subdued.

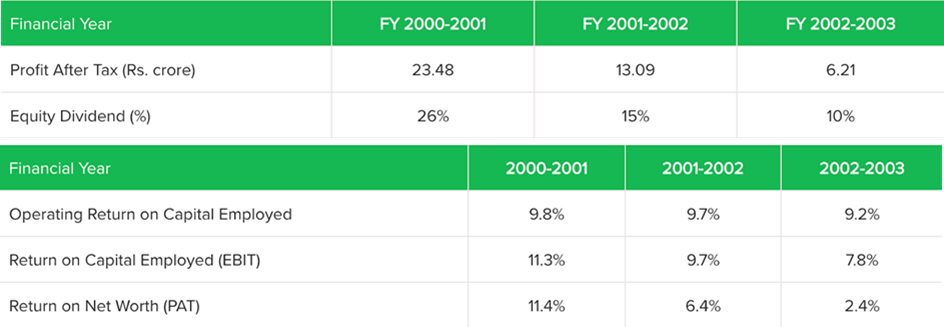

This resulted in an evident decline in profitability and operating metrics as shown below:

Asset under discussion

Titan Company Ltd

15

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~400 views

3/n With an extended list of obstacles and pessimistic foresight, the share dropped to an 8 year low of Rs. 29.

But, it was now, when the share was between Rs. 30 - 35 that RJ started to buy! 🐂

Why did he buy? Here’s the breakdown…

3

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~780 views

4/n

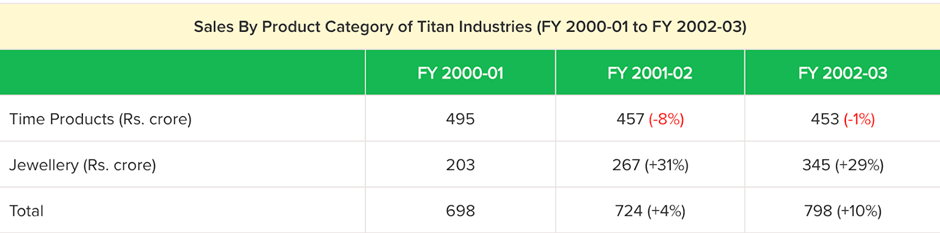

Firstly, a deeper analysis of the sales number for $Titan Company Ltd showed a different picture. Even during the most troublesome times (2001-2003), Titan’s Jewellery business grew approximately 30% and Tanishq opened 52 stores across the country!

There was a strategic indication from the management towards pushing the Jewellery segment.

Asset under discussion

Titan Company Ltd

4

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~790 views

5/n

Internally, the company undertook some decisive restructuring changes as well:

1. A Voluntary Retirement Scheme for 600 employees

2. Restructuring the company’s European operations

3. Projects to help reduce the working capital requirement

But this was not all. Jhunjhunwala saw something else in $Titan Company Ltd FY 2002-03 annual report as well!

Asset under discussion

Titan Company Ltd

4

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~790 views

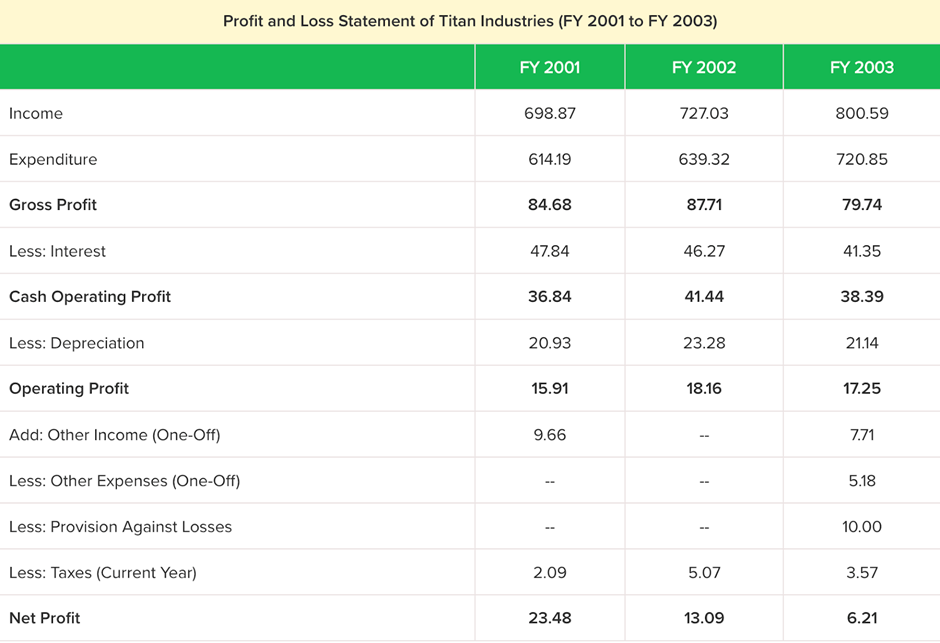

6/n Interestingly, an analysis of the annual report showed that the decline in profitability in FY 2003 was due to a Rs. 10 crore provision against losses set aside for the restructuring of the European operations.

Furthermore, the company’s operating profit was in fact stable in a range between Rs. 16 crore to Rs. 18 crore for the fiscal period 2001-2003. This underscored the company’s operational stability. $Titan Company Ltd

Asset under discussion

Titan Company Ltd

6

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~760 views

7/n

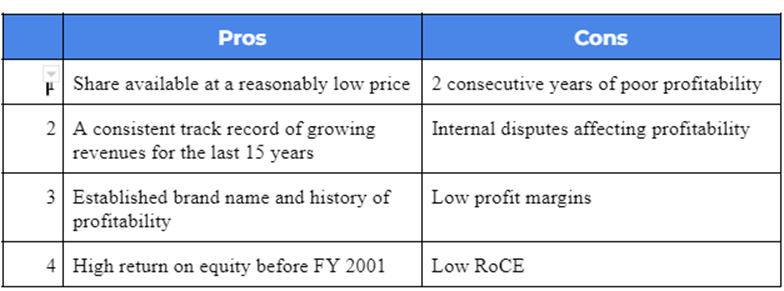

Jhunjhunwala was able to cut through the clutter and read into the fine print of $Titan Company Ltd financial and operational reality. And, this is broadly what he might have visualized:

Asset under discussion

Titan Company Ltd

5

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~810 views

8/n This enabled him to come up with insights which not only differentiated him from the herd, but, more importantly, allowed him to buy and hold the stock with strong conviction.

And, the rest is of course history!

A good way to confirm if $Titan Company Ltd was an investable business is through Ben Graham’s Net Current Asset Value Method. Here’s how it works..

Asset under discussion

Titan Company Ltd

4

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~440 views

9/n The first step is to understand the 4 components which you can get from a company’s balance sheet: 1. Net Current Assets of the company 2. Amount of Preference Share Capital 3. Long-Term Debt of the company 4. Total Number of Outstanding Equity Shares

Then, we can calculate the Net Current Assets (NCA) per share of the company: (Current Asset - Current Liab)/ No. of shares

In Titan’s case, as of 31st March 2003, NCA were Rs. 396 crore. And, at this time Titan had 4.22 crore outstanding shares.

On 31 March 2003, the closing price of Titan was Rs. 50 but, using this we get NCA per share to be Rs. 93.84 on the same date. This indicated the Titan’s NCA liquidation value was 2x the market cap. Such a difference assures investors that there is a significant safety margin!

4

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~820 views

10/n

Now, the formula to calculate Net Current Asset Value (NCAV) of a stock is like this: NCAV = [(Net current assets – Preference share capital) – Long Term Debt] / Total Equity Shares

From $Titan Company Ltd ’s balance sheet for the year ending 31 March 2003, we get the following data: - Net Current Assets = Rs. 396 crore - Preference Share Capital = Rs. 40 crore - Long Term Debt = Rs. 467 crore - Number of Equity shares = 4.22 crore

This resulted in Titan’s NCAV for 31 March 2003 = (-)Rs. 26.30

One must think that by this method, Titan is not an investable stock..

Asset under discussion

Titan Company Ltd

4

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~450 views

11/n

But, the reason for this is that Graham’s formula was based in the mid 1900s when companies did not rely on borrowings. This would have meant that NCA would be much higher than market cap or debt.

Thus, to make it relevant, we must adjust it for more recent times. Assume that you will need to buy all shares and pay off a company’s debt to buy it:

Amount Required to Buy a Company = Debt + Market Cap

Now, the revised formula we can use would look like this:

Easily Accessible Money By the Company / Amount To Buy Entire Company = (Net Current Assets – Preference Share Capital) / (Market Cap + Debt)

From Titan’s balance sheet for 31 March 2003, this ratio comes to 53%. This represents the liquid assets of Titan at the end of FY 2003.

At this point, we haven’t even included the long term factors of the company. If we were to add things such as land, cash-flow, and growth prospects, Rs. 50 would be a very lucrative price to buy Titan! Yes big money thinks like a businessman.

5

0

1

Rakesh Jhunjhunwala - Fan page

@rjhunjhunwala

3 years ago ~810 views

12/12 So what did we learn from RJ's phenomenal journey in $Titan Company Ltd :

1. To be a good investor, one needs to understand the fine print of the financial statements of a company and learn to read between the lines. 2. Internal and external factors which are not operational or fundamental in nature have nothing but a temporary impact on the stock price of a company. 3. Using deep tools such as Net Current Asset Value allows investors to come up with insights that result in exceptional returns compared to the market.

Hope you learnt something new in this thread. Share with friends if you did. Have a good weekend.